Maggiori informazioni sul libro

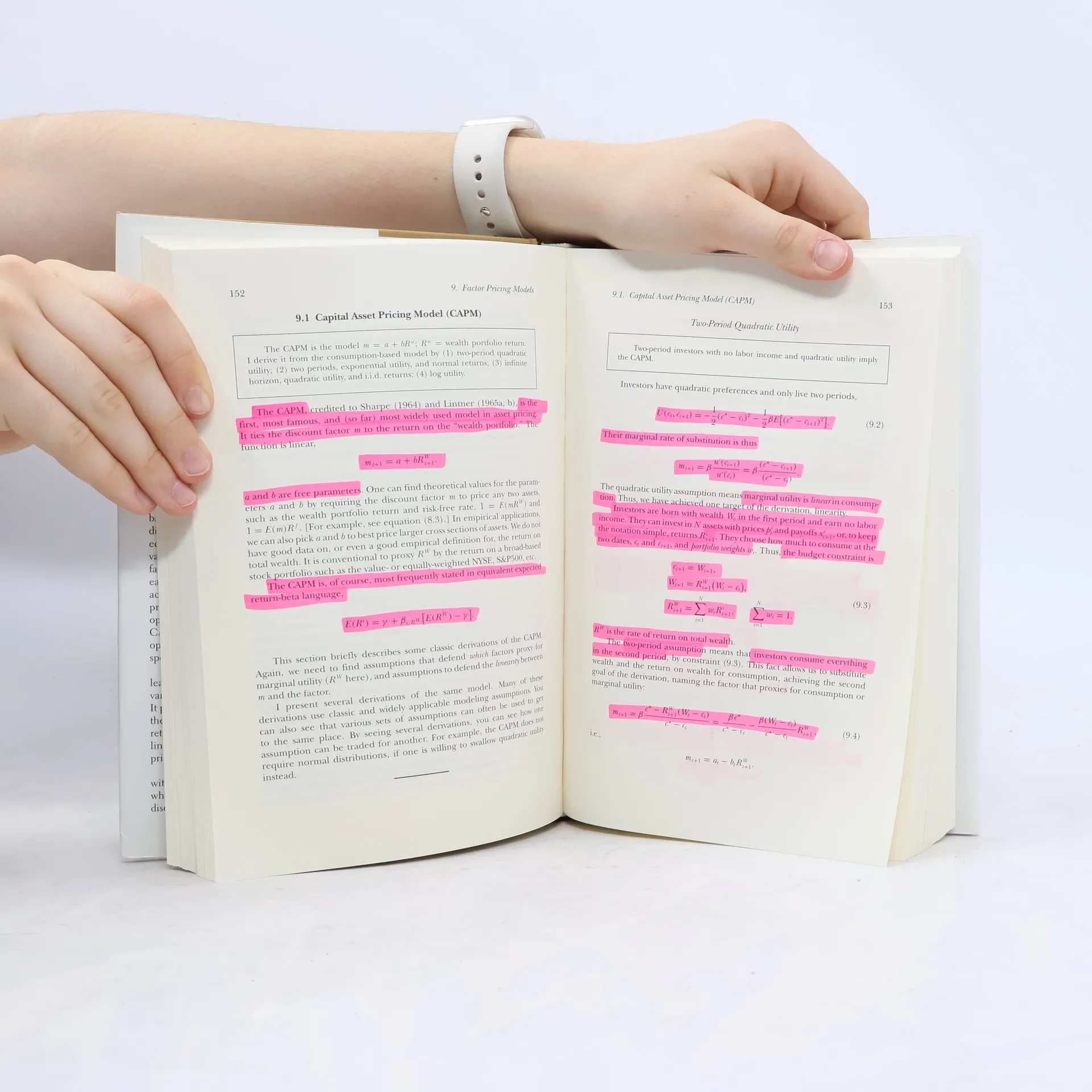

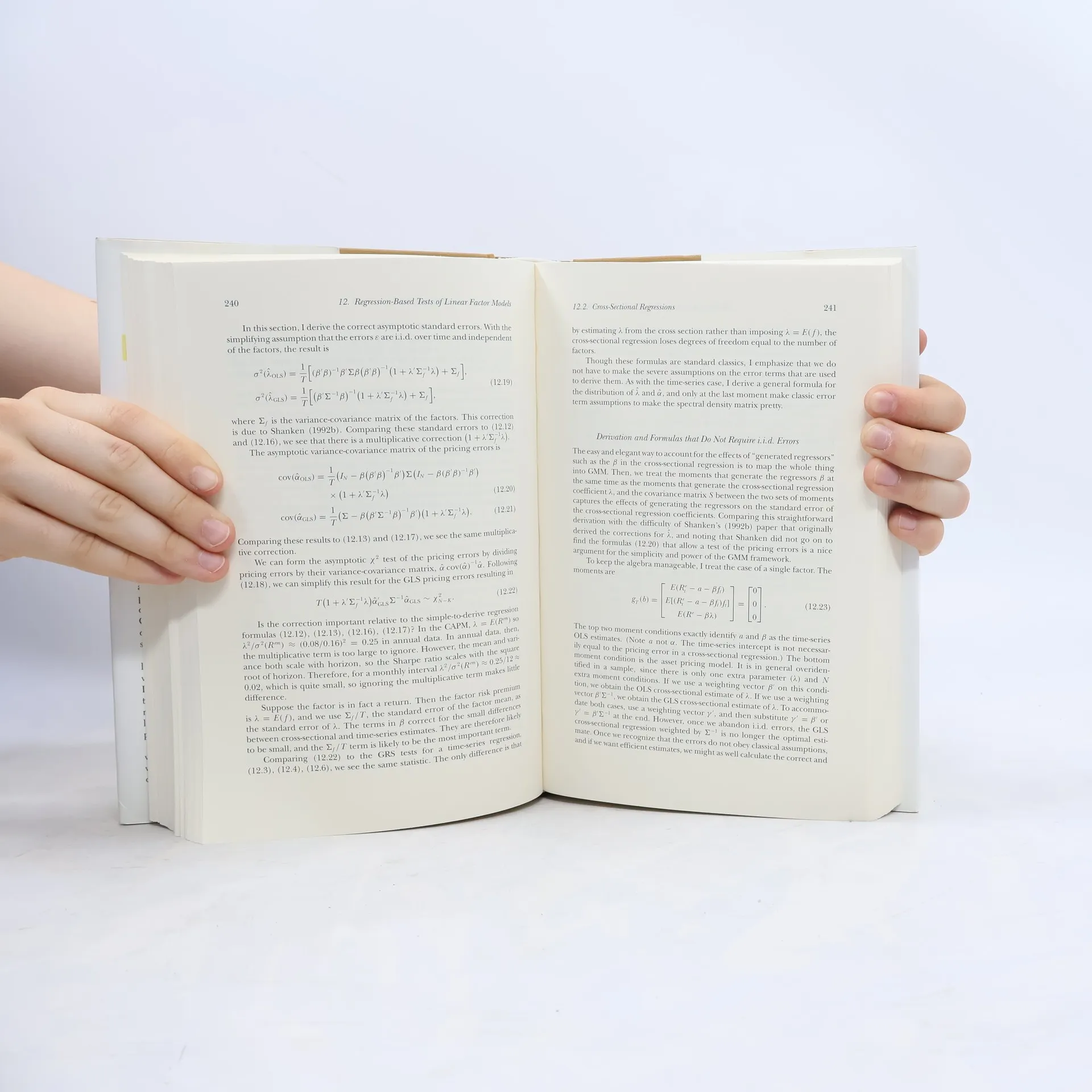

Winner of the Paul A. Samuelson Award, John Cochrane's revised edition of Asset Pricing unifies and modernizes the science of asset pricing for advanced students and professionals. Cochrane connects the pricing of all assets to a core concept: price equals expected discounted payoff, reflecting the macroeconomic risks of each security's value. By employing a single stochastic discount factor, he constructs a cohesive framework applicable to stocks, bonds, and options. Each model—consumption-based, CAPM, multifactor, term structure, and option pricing—is presented as a variant of this discounted factor. This framework also introduces a state-space geometry for mean-variance frontiers and asset pricing models, positioning payoffs in various states of nature on the axes, which results in a new linear representation of asset pricing concepts. Cochrane employs the Generalized Method of Moments (GMM) to analyze sample average prices and discounted payoffs, verifying the fundamental relationship between price and expected discounted payoff. He adeptly navigates between discount factor, GMM, and state-space language, as well as the beta, mean-variance, and regression terminology prevalent in empirical studies. Additionally, the book reviews contemporary empirical research on return predictability, value and other cross-sectional puzzles, and the equity premium puzzle and its solutions. Designed as both a summary for academics and pr

Acquisto del libro

Asset Pricing, John H. Cochrane

- Lingua

- Pubblicato

- 2005

- product-detail.submit-box.info.binding

- (Copertina rigida),

- Condizioni del libro

- Danneggiato

- Prezzo

- 11,92 €

Metodi di pagamento

Ancora nessuna valutazione.

- Titolo

- Asset Pricing

- Sottotitolo

- Revised Edition

- Lingua

- Inglese

- Autori

- John H. Cochrane

- Editore

- Princeton University Press

- Pubblicato

- 2005

- Formato

- Copertina rigida

- Pagine

- 568

- ISBN10

- 0691121370

- ISBN13

- 9780691121376

- Serie

- Tag

- Saggistica, Libri di testo, Commercio, Business & Management, Manuali e guide, Economia, USA, Finanza, Denaro, Titoli di valore

- Descrizione

- Winner of the Paul A. Samuelson Award, John Cochrane's revised edition of Asset Pricing unifies and modernizes the science of asset pricing for advanced students and professionals. Cochrane connects the pricing of all assets to a core concept: price equals expected discounted payoff, reflecting the macroeconomic risks of each security's value. By employing a single stochastic discount factor, he constructs a cohesive framework applicable to stocks, bonds, and options. Each model—consumption-based, CAPM, multifactor, term structure, and option pricing—is presented as a variant of this discounted factor. This framework also introduces a state-space geometry for mean-variance frontiers and asset pricing models, positioning payoffs in various states of nature on the axes, which results in a new linear representation of asset pricing concepts. Cochrane employs the Generalized Method of Moments (GMM) to analyze sample average prices and discounted payoffs, verifying the fundamental relationship between price and expected discounted payoff. He adeptly navigates between discount factor, GMM, and state-space language, as well as the beta, mean-variance, and regression terminology prevalent in empirical studies. Additionally, the book reviews contemporary empirical research on return predictability, value and other cross-sectional puzzles, and the equity premium puzzle and its solutions. Designed as both a summary for academics and pr